The globe is currently in the midst of a pandemic related to the Coronavirus and COVID-19, the disease it causes. This pandemic is meaningfully impacting economic and financial market activity throughout the world. The ongoing magnitude and duration of these effects is highly unknown, though it is very reasonable to assume market volatility will continue until the situation is mitigated. That is not to surmise stock or bond markets will necessarily go higher or lower. Rather the day-to-day movement of these markets will likely be larger than historical averages.

The purpose of this memo is to provide you, our valued WoodTrust client, background and information on how we’re continuing to monitor and manage your investment portfolio. The strategies outlined below are utilized regularly with client portfolios and become particularly important during times of market stress.

This memo, however, is not intended to speak to updates of current events. The situation is far too fluid and evolving minute-by-minute. Further, this memo is not intended to speak to the operating functions of WoodTrust Bank or WoodTrust Asset Management. Additional information related to that will be available at www.woodtrust.com and updated there regularly as information changes.

While global equity and fixed income markets have proven volatile over the last number of days, these meaningful declines in the stock market can be expected from time to time. In fact, when viewed in a historical context, the average intra-year decline for the S&P 500 Index since 1980 exceeds 14%. Nevertheless, volatility is not an excuse for apathy. There are four time-tested solutions that can improve portfolio performance over the long-run:

1) Focusing on asset allocation

2) Disciplined portfolio rebalancing

3) Opportunistic tax-loss harvesting

4) Mastering one’s emotions

Solution 1: Focusing on Asset Allocation

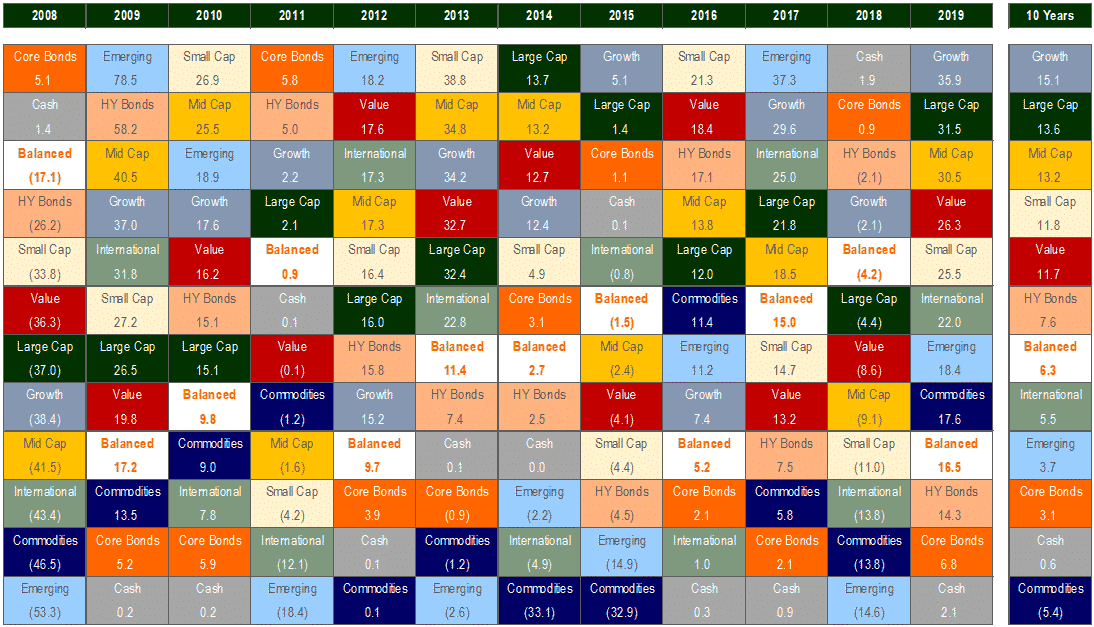

There is an understandable fallacy that exists in today’s high-energy, short-term focused financial press that market timing and always investing in the hottest stocks is the secret for success. This is perpetuated by the feeling (perhaps better stated as a long-shot hope) that picking the perfect time to enter or exit the market or picking the next high-flying stock will guarantee substantial wealth creation. The theory here is if one can master this, then good old-fashioned planning, saving, and watching expenses can be ignored. Unfortunately, this is the rare exception and far from the norm. In reality, for most investors, the biggest factor in determining long-term success has been, and will always continue to be, asset allocation.

Simply stated, asset allocation is investing your money in different categories of assets such as stocks, bonds, and cash so your portfolio is well diversified. Ultimately, the objective of a good asset allocation plan is to develop an investment portfolio that will help reach financial objectives with the degree of risk that is comfortable and consistent with your well-developed and disciplined strategy. A well-diversified portfolio may not outperform the top asset class in any given year, but over time it can be an effective way to realize long-term goals. From year-to-year, it is impossible to consistently predict how each individual asset class will perform – a strong argument for consistent portfolio diversification.

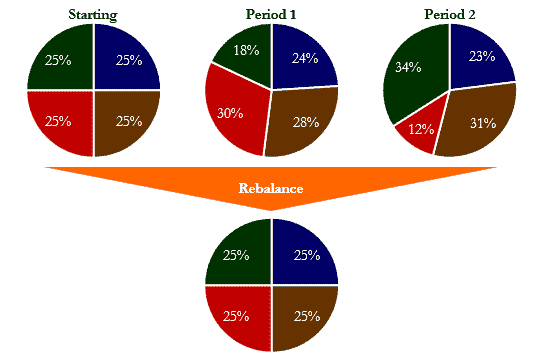

Solution 2: Regular Portfolio Rebalancing

Over time, certain investments in a diversified portfolio will grow more or decline less than others, which can cause actual allocations to shift away from initial targets. As a result, the portfolio will end up either taking on more risk than intended, or not pursuing its goals as aggressively as one would have liked. Portfolio “rebalancing” is critically important because it helps investors maintain their target asset allocation. By periodically rebalancing, investors can diminish the tendency for “portfolio drift,” and reduce their exposure to risk relative to their target asset allocation over time.

When a portfolio is rebalanced, it sells a small portion of the historical, backward-looking “winners” and buys a small portion of the historical “losers”. Importantly, these are marginal moves that are not extreme in nature. It is common following significant declines in the equity markets, such as now, for investors to question the benefits of rebalancing. Understandably, during times of extreme volatility, weak investment performance coupled with uncertainty about the future make it difficult for investors to rebalance their portfolios by trimming their best-performing asset classes and committing more capital to underperforming asset classes. However, historically, significant rebalancing opportunities present themselves after significant, negative market events. Investors who fail to rebalance their portfolios during times of stress, though rebalancing is equally as important in strong positive markets, may not only miss out on the subsequent return to normalized market pricing, but they will also not maintain the desired asset-class exposures charted in their targeted, risk-based asset allocation.

Solution 3: Opportunistic Tax-Loss Harvesting

Within taxable accounts, selling investments that have lost value can be a useful tax-reduction strategy for investors in any particular tax year, but the practice is especially attractive during volatile markets. This strategy, called tax-loss harvesting, refers to selling stocks, bonds, or other securities that have temporarily lost value to help reduce taxes owed – now or in the future – on capital gains realized from winning investments.

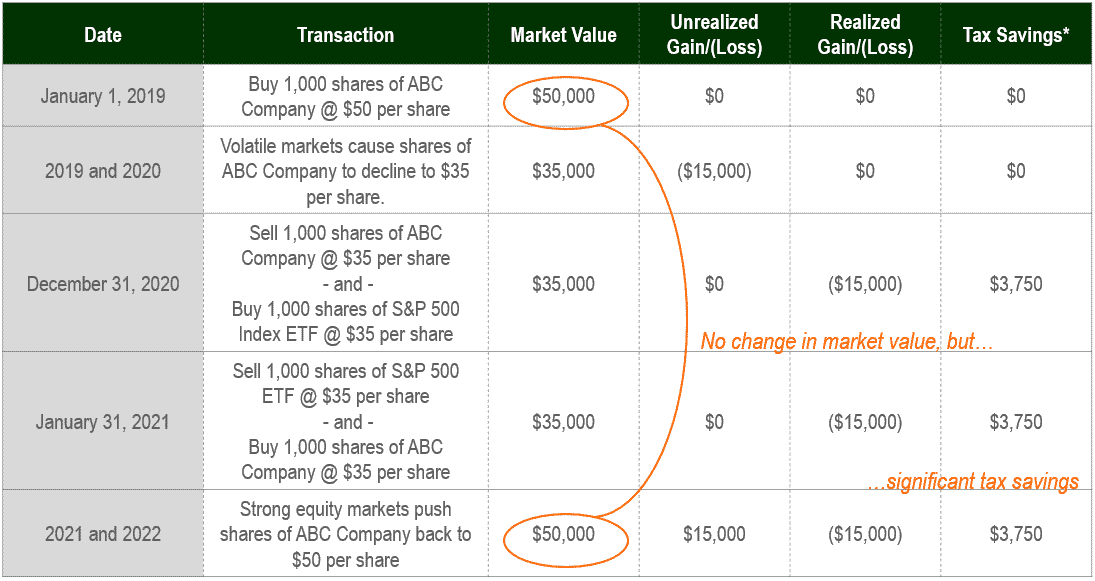

Opportunistic tax-loss harvesting can reduce taxable income and save money. In the example below, the investor purchased ABC Company stock, which subsequently declined in value. A tax-loss harvesting strategy was employed to sell the security, realize the loss for tax purposes, and purchase a market index ETF as a temporary placeholder to maintain the portfolio’s asset allocation. After at least 30 days, the investor repurchased their shares of ABC Company to return the portfolio to its original allocation, while also realizing the tax loss. Through completion of this process, the portfolio’s market value remained unchanged, though the investor saved significantly on taxes.

Solution 4: Mastering One’s Emotions

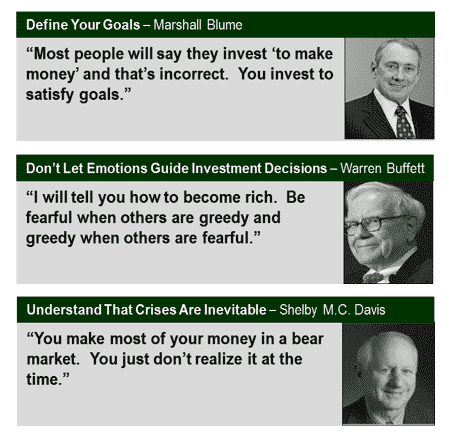

It is only natural that, with sharp negative volatility in the stock market, investors of all types become uncertain. During periods of extreme uncertainty and market turmoil investors often make impatient, emotional decisions that undermine their ability to reach their long-term investment and financial goals. The risks of large incorrect asset allocation changes based on short-term information can permanently impair the long-term performance of a portfolio and the achievement of goals.

While disruptive markets are not always welcomed, they should be anticipated and appropriately prepared for. When times of uncertainty do arise, to the extent possible, they can be used as an opportunity to rebalance portfolios (see Solution 2) and prepare for the future. This approach borrows the wisdom of great investors as a guide to navigating constantly evolving markets.

In Summary

Markets will always go through periods of turmoil and uncertainty. There will be periods of economic recession and growth, there will be periods of global conflict and calm, and there will be periods of revolutionary changes in the way we live. What is difficult, if not impossible, to do is predict the timing and impact of change. It is important that investors have a disciplined plan that meets their unique needs, thereby avoiding the destructive behavior of pundits and short-term market timers. Investors can benefit from staying the course and utilizing time-tested solutions that improve long-term portfolio performance such as focusing on asset allocation, rebalancing, tax-loss harvesting and mastering one’s emotions.

WoodTrust Asset Management Investment Committee

Chad D. Kane – President

Jason T. Deitz, CFA – Senior Vice President & Chief Investment Officer

D. Mike Glodosky, CTFA – Senior Vice President & Portfolio Manager

Jon R. Clark – Vice President & Portfolio Manager

Marc P. Kettleson, AFIM – Vice President & Portfolio Manager

Terry J. Knoll, CFP, CRSP – Vice President & Portfolio Manager

Michael J. Spalding, CFA – Vice President & Portfolio Manager

Justin J. Regnier, CFA – Portfolio Manager

Recent Comments